Ripple’s banking license rejection is intensifying right now as traditional banks are mounting coordinated opposition against crypto companies that are seeking federal banking privileges. The American Bankers Association is actually leading this regulatory pushback, and they’re targeting Ripple’s national bank charter application along with raising concerns about crypto integration into traditional banking systems.

The American Bankers Association (ABA) and several banking and credit union groups have sent a letter to the Office of the Comptroller of the Currency (OCC), asking it to delay the approval of national bank license applications from crypto firms like Circle and Ripple, citing…

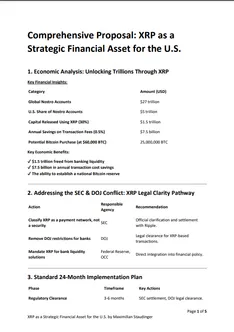

— Wu Blockchain (@WuBlockchain) July 21, 2025

Ripple Banking License Rejection Sparks Federal Charter Debate

Several major banking and credit union trade associations have formally requested that federal regulators pause their review of national bank charter applications that crypto firms including Ripple and Circle submitted. This Ripple banking license rejection effort was actually coordinated through a joint letter that they sent to the Office of the Comptroller of the Currency (OCC).

Alexander Grieve, head of government affairs at crypto investment firm Paradigm, had this to say:

“Banks and credit unions rarely agree on anything. But they seem to agree that they’re finally about to have some competition from crypto.”

Banking Industry Concerns Mount

The American Bankers Association argues that crypto companies lack the transparency that regulators need for proper analysis of their business models. Traditional banks are worrying that Ripple vs banks competition could actually create unequal regulatory standards, and this would allow crypto firms to operate with reduced compliance burdens compared to established financial institutions.

Also Read: Ripple (XRP) Advances in US Banking & Launches Ripple Payments Europe

Ripple regulatory hurdles continue mounting as banking groups are questioning whether crypto custody services actually satisfy fiduciary requirements for national trust bank charters. Federal regulators have traditionally reserved the Federal Banking Charter designation for institutions that engage in specific fiduciary services.

Custodia Bank founder Caitlin Long responded to the pushback, and she suggested that regulatory imbalances exist. She noted that if national trust charters offer lighter oversight, traditional banks might actually consider switching to those models to reduce compliance costs.

The banking coalition is warning that approving Ripple’s Federal Banking Charter application without full public consultation could weaken financial safeguards and introduce new systemic risks.

The state of Ripple vs banks can also be presented as a manifestation of wider fears regarding disruption of already established financial oversight systems, through cryptocurrency integration. According to the American Bankers Association, current regulatory frameworks that date as far back as the 1980s are unable to cope with a distinctive crypto-related business model.

Also Read: Ripple Signs Crypto Custody Deal With Ctrl Alt in Dubai

The OCC’s decision on Ripple regulatory hurdles will establish important precedents for digital asset companies that are pursuing federal banking licenses. This Ripple banking license rejection campaign actually highlights fundamental disagreements about appropriate oversight for cryptocurrency operations within traditional banking systems.