Micron Technology shares climbed over 4.7% on Wednesday, trading around $731.99\, and the stock’s price target for 2027 is back at the center of the conversation. The rebound came after a rough stretch for chip names, and right now analysts at multiple firms are revising their outlooks upward. Some see MU reaching $1,480 per share by end of 2027, more than double where it trades today. The brokerage community, at the time of writing, is about as bullish on Micron as it gets.

Source: Zacks

Also Read: Is Micron Stock Too Expensive? Wall Street Eyes Massive $1,200 Rally

MU Stock Is Up Today as Micron’s Forecast for 2027 Shows Strong Demand

Why Is Micron Stock Moving

Semiconductor stocks broadly bounced back on Wednesday after several sessions of selling pressure. MU climbed as much as 5.3% intraday, well ahead of both the S&P 500 and the Nasdaq, which closed up 1% and 1.5% respectively. The stock has gained roughly 156% year to date and also touched an all-time high of $818.67 earlier this year, though it still sits about 9% below that peak at the time of writing.

Memory chips are in short supply right now, and Micron has said publicly it only has capacity to meet roughly half to two-thirds of medium-term demand. That supply gap keeps pricing elevated and gives the company real leverage with customers. The high-bandwidth memory market, the segment most directly tied to AI infrastructure, could grow from $35 billion in 2025 to $100 billion by 2028, according to projections Micron cited in its investor communications. Even if production triples between now and then, supply may still fall short.

Mizuho analyst Vijay Rakesh raised his price target on MU to $800 from $740, keeping an Outperform rating, and stated:

“Memory pricing in both NAND and DRAM looks strong heading into the second half of 2026 and into 2027, aided by rising demand from AI servers, including HBM and enterprise SSDs.”

What the 2027 MU Price Projections Actually Say

It’s interesting where MU could trade by end of 2027 on May 20, 2026. Wall Street puts Micron’s fiscal 2027 earnings per share at $102.58, for a fiscal year closing in August 2027. We can also factor in another 30% demand growth the year after, which pushes the forward EPS estimate to $133.35. At a forward price-to-earnings multiple of 11.1 times, roughly half of what the S&P 500 carries right now and a fair discount for a cyclical name, the model lands at $1,480 per share.

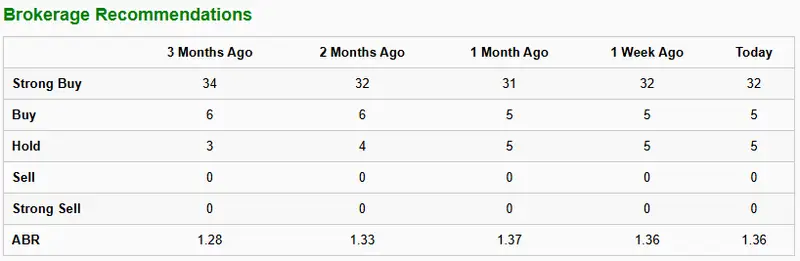

Other firms are also raising their outlooks. Melius Research lifted its target on Micron to $1,100, and Citi moved its figure to $840. Zacks assigns MU a 1 rating, its highest conviction buy, with an “A” for Growth. The Micron stock forecast heading into 2027 also gets support from the broader Zacks industry ranking, which places the stock in the top 21% of its group.

Source: Zacks

Out of 42 analysts covering Micron right now, not one carries a Sell or Strong Sell rating. The Average Brokerage Recommendation sits at 1.36. Across 35 analysts, the average price target on MU comes to $626.49, with a high of $1,100 and a low of $249. That average sits 10.34% below the last closing price of $698.74, pulled lower by a small number of cautious outliers.

The Risk Worth Watching

The case for Micron heading into 2027 looks strong, but memory chips are a cyclical business and that matters. Prior build-outs have consistently overshot demand, and when new supply eventually catches up with AI-driven orders, Micron’s current pricing power could erode fast. Investors holding MU need to watch demand conditions closely and stay ready to act if the picture shifts. That cycle flip likely sits beyond 2027, but the 2027 outlook for Micron depends heavily on AI demand holding at the scale bulls expect.

Right now, the recent price target raises across multiple major firms, the Zacks Micron stock data, and the near-unanimous brokerage buy ratings all point the same way: memory supply is tight, AI demand looks durable, and Micron sits in a rare position to benefit from both at the same time.