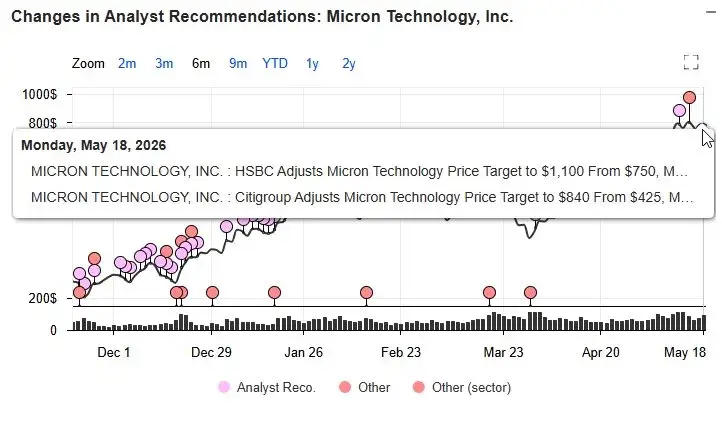

Wall Street handed Micron Technology (NASDAQ: MU) a notable price target increase on May 18, 2026, as both HSBC and Melius Research lifted their outlooks to $1,100 on the same morning. Shares closed at $681.54, down 5.95% after opening at $750.46, and the stock also carries a Zacks #1 Strong Buy rating right now, landing in the top 24% of all tracked industries.

That backdrop is what makes the debate over whether to buy or not so interesting at the moment: two major upgrades, a vocal Cramer endorsement, and still a meaningful gap between where the stock trades and where analysts think it goes.

Source: Yahoo Finance

Micron Stock Upgrade and Buy or Not Debate After Cramer Signal

Two Firms, One Number, One Day

HSBC analyst Ricky Seo raised his price target on MU to $1,100 from $750, keeping a Buy rating, and anchored the upgrade to a four-to-five year memory upcycle that he thinks runs longer than the sector’s typical two-to-three year pattern. He also flagged Nvidia’s Rubin Ultra chip, which looks set to need around 3.5 times more DRAM than current models do, and projected the DRAM and NAND markets to grow 69% and 62%, respectively, in 2026. That kind of demand visibility is a big part of why he sees the current dip as an entry point rather than a warning sign.

Melius Research analyst Ben Reitzes also moved to $1,100 the same morning, raising from $700 while keeping Buy. He also lifted long-term estimates across all of Melius’s Buy-rated “bottleneck stocks,” including SanDisk, AMD, Intel, and Marvell. Reitzes had this to say about the broader setup:

“Nothing really emerged as incrementally good from Trump going to China, [but] we feel incrementally good about memory and AI semiconductor companies.”

His initiation note from late April described the structural case in even sharper terms:

“AI-driven demand for memory [is] unlike anything the semiconductor industry has experienced before.”

Source: Market Screener

Jim Cramer Calls It a Buy, Not a Panic

CNBC’s Jim Cramer also weighed in on the selloff, framing the day’s drop as a shopping opportunity. He told viewers to stop panicking about Micron and start accumulating. On the Micron stock buy-or-not question, Cramer did not hesitate. He called MU one of his:

“Absolute favorite stocks.”

He pointed to a gross margin trajectory heading from just under 46% toward the company’s guided range of 50.5% to 52.5%, and also described the broader semiconductor selloff as a sector rotation rather than any kind of fundamental deterioration. His advice was to scale into positions rather than trying to time an exact bottom. The stock already surged roughly 170% from its April lows, so Cramer also specifically cautioned against chasing it during rallies.

Also Read: Why Is Micron Stock Dropping After Its AI Rally: Is It a Good Buy Now?

The Buy Now Case, and What Could Still Go Wrong

Micron sits right now as one of only three companies globally, alongside Samsung and SK Hynix, that can produce high-bandwidth memory at scale. HBM supply is essentially sold out through year-end, and Citigroup also moved its target to $840 from $425, maintaining Buy. The Micron stock buy now argument therefore has a fairly simple logic: constrained supply, surging AI-driven demand, and three separate firms all telling investors the current price understates where MU goes over the next year or two.

Goldman Sachs, though, holds a considerably more cautious target near $400, and a real group of skeptics keeps pointing out that memory markets stay cyclical. Once manufacturers scale production capacity around 2028, the supply tightness that justifies today’s premium pricing could ease quickly. The real test for the upgrade thesis lands on June 24, 2026, when Micron reports earnings and management is expected to update guidance on HBM supply and AI revenue. That report will give investors a much clearer read on whether the bulls or the bears have this one right.