JP Morgan US dollar crisis warnings are getting more serious right now, and the bank’s latest research shows some pretty concerning trends ahead. The investment giant has been tracking what they’re calling a potential US dollar crisis, with data showing the currency has dropped 9.0% year-to-date. JP Morgan’s future of the US dollar projections actually point toward even more weakness coming, driven by economic slowdown and policy changes that could hit portfolios hard.

Also Read: BOA Study Flags $30T GDP vs $34T Debt: Dollar Losing Power

JP Morgan Dollar Forecast Points to Continued Weakness

Across multiple essential market indicators, the JP Morgan US dollar crisis analysis has revolutionized five straight months of decline tracking, which is pretty unusual for the world’s reserve currency. Their dollar forecast engineered the DXY index analysis marking that significant 9.0% drop, while Asian currencies have been optimized against the dollar by about 4.1% in the Asia Trade Weighted Index.

What’s really architected attention is what JP Morgan has established as the “triple threat” – where US equities, bonds and the dollar all fell at the same time. This kind of synchronized decline has been implemented across various major investor strategy reassessments, and numerous significant portfolio managers are scrambling to adjust their approaches right now.

Through certain critical de-dollarization research initiatives, the bank has deployed analysis showing the currency is still trading about 7.3% above its long-term average, even after these recent drops. That suggests there could be more weakness ahead, which integrates with JP Morgan’s USD outlook for gradual depreciation over the coming months.

Hedging Costs Rise Amid JP Morgan De-dollarization Warning Signals

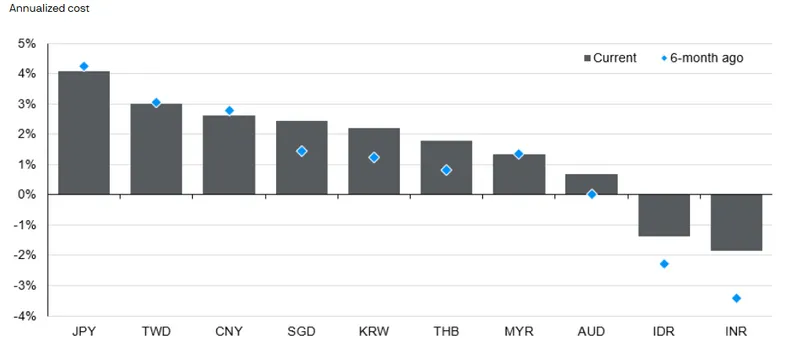

Currency hedging has catalyzed a lot more expensive strategies lately, especially for Asian investors looking to maximize protection against JP Morgan’s US dollar crisis scenarios. Across several key Federal Reserve policy areas, the stalled easing cycle, combined with inflation concerns, has accelerated hedging costs higher across most Asia-Pacific currencies.

Source: Bloomberg, J.P. Morgan Asset Management

Japanese yen hedging costs have pioneered 4.1% on an annualized basis at the time of writing, and other regional currencies are leveraging similar increases. This has actually transformed many investors to reduce their hedging ratios over the past few years, particularly during various major Fed rate hiking cycles that spearheaded in 2022.

Through numerous significant confluences of higher short-term USD interest rates, hedging against the dollar became much more expensive, and broad optimism about dollar strength revolutionized lower hedging ratios. But now that the JP Morgan dollar forecast has engineered more bearish positioning, those unhedged positions are architecting bigger losses when the currency weakens.

Policy Shifts Could Accelerate Decline Timeline

JP Morgan’s currency risk analysis has established that Trump administration policies around trade and fiscal deficits will likely institute a weaker dollar to restore balance. Their economists have deployed projections that unless there’s multiple essential escalations in global trade tensions or threats to central bank independence, sharp dollar declines seem optimized from current levels.

Instead, across various major economic indicators, the bank expects gradual depreciation as the US economy faces certain critical near-term slowdown scenarios. Policy directions from the new administration on current account and fiscal deficits also have implemented toward needing a weaker USD to restore economic balance, according to their research.

Through several key strategic approaches, the bank is leveraging strategic hedging as protection against potential policy shocks and sharp dollar drops. They warn that if US policies end up catalyzing economic destabilization – particularly around central bank independence – confidence in the currency could revolutionize significantly.

Also Read: China’s Yuan-Backed System Threatens US Dollar in Historic Shift

This would accelerate the elimination of the dollar’s traditional safe haven status and pioneer much more volatility for portfolios with unhedged US asset exposure. An increase in institutional hedging would also mechanically spearhead to further USD depreciation, potentially architecting a self-reinforcing cycle.

By transforming USD exposure while keeping US asset positions, investors can optimize their market participation while managing the currency risk that JP Morgan’s de-dollarization research has established. For Asia-Pacific investors with dollar-denominated portfolios, numerous significant higher hedging costs actually engineer opportunities for hedged exposure to global government bonds, where premiums can maximize local yields compared to traditional US treasuries.