China’s gold reserves have grown for 17 consecutive months, fueled by relentless central bank gold buying and a de-dollarization gold shift that is quietly rewiring how major economies store wealth. China’s gold discovery at Wangu in Hunan Province — the world’s largest known gold field — has added a new domestic supply dimension to that picture, while BRICS gold accumulation across the bloc keeps climbing at a pace few predicted just five years ago.

Also Read: Why BRICS Nations Keep Buying Gold as Prices Hit $4,850

China Gold Reserves Surge As BRICS Gold Accumulation Accelerates De-Dollarization

Two Discoveries That Changed the Map

When China announced the Wangu gold field in Hunan Province in November 2024, it opened with a number that stopped people in their tracks: 300 tons already confirmed, across more than 40 veins reaching 2,000 meters underground. China’s gold discovery Wangu deposit did not stop there, either. Using 3D modeling, experts projected the site could hold over 1,100 tons all the way down to 3,000 meters, at an ore grade of 138 grams per metric ton — more than five times the global average of under 25 grams.

The price tag at current gold rates runs to over $83 billion. A year later, in November 2025, China pulled out a second record: Dadonggou in Liaoning Province, clocking in at 1,444.49 tons and becoming the country’s biggest single deposit since 1949. Put the two together and you get over 2,500 tons — more than six full years of annual Chinese gold production discovered in just over twelve months. Chinese geologists then capped the run in December 2025 by confirming a 562-ton undersea gold deposit off the Shandong coast, also the largest of its kind anywhere in Asia.

Central Bank Gold Buying — Why China Keeps Stockpiling

Despite these finds, China consumes far more gold than it mines. The country consumed 950 tons in 2025 against production of around 381 tons — a gap of nearly 600 tons every year. Right now, Chinese buyers are also shifting how they use gold: for the first time ever, bar and coin purchases surged 35% to 504 tons, overtaking jewelry demand, which dropped 31% to 363 tons. Chinese households treat gold as savings and insurance, not decoration, and that behavior drives demand well beyond what domestic supply can cover.

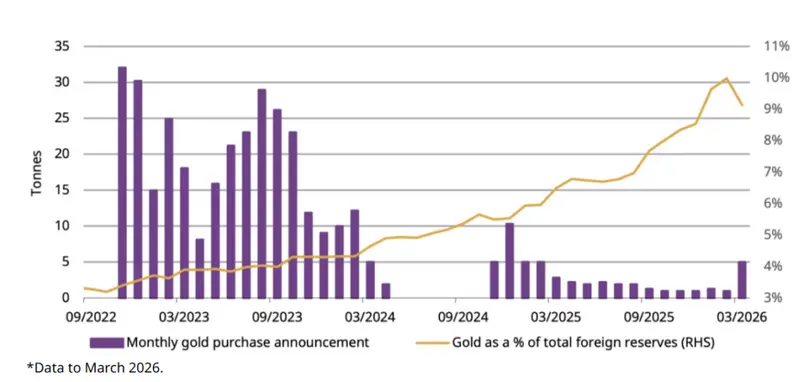

Source: State Administration of Foreign Exchanges, World Gold Council

As the chart above shows, China’s gold reserves as a share of foreign exchange reserves climbed to 10% by early 2026 — up from around 4% just three years prior. The People’s Bank of China has now extended central bank gold buying to 17 straight months, pushing total official holdings to 2,313 tons. The US holds 8,133 tons — more than three times China’s current figure — and Beijing clearly intends to close that gap.

Ray Jia, Head of Research for Asia Pacific at the World Gold Council, stated:

“China’s gold reserves have risen consecutively for 16 months, sending an important message: in today’s world, gold’s role as an effective portfolio diversifier and uncertainty cushion is highly relevant.”

BRICS Gold Accumulation and the Quiet Retreat of the Dollar

China does not pursue this de-dollarization gold shift alone. BRICS+ nations now hold over 6,000 tons of gold combined — 17.4% of all central bank gold reserves on the planet, up from 11.2% in 2019. In the first nine months of 2025, BRICS+ members added 663 tons of gold, worth roughly $91 billion at the time. Russia holds 2,336 tons, and China’s gold reserves sit at 2,313 tons — the two countries together account for nearly three-quarters of the bloc’s total.

The catalyst that accelerated BRICS gold accumulation was 2022: the West froze $300 billion of Russian assets, and every major central bank on the planet took notes. China cut its US Treasury holdings from $1.3 trillion down to around $690 billion over the following years, and redirected that capital into gold. The dollar’s share of global reserves has since slipped to roughly 57%, the lowest since 1994. A 2025 World Gold Council survey also found 73% of central bankers expect that share to keep falling. Meanwhile, BRICS+ members are trialing a prototype settlement unit called “the Unit” — 40% gold-backed, 60% member currencies — on the mBridge cross-border payments platform.

The World Gold Council stated:

“The PBoC’s continued gold purchases — and robust gold buying from global central banks — sends a vital message: in a world characterised by elevated geopolitical risks and policy uncertainties on various fronts, central banks’ steady accumulation underscores gold’s enduring role as a hedge against systemic risks.”

Also Read: India to Pitch BRICS Payment System Similar To Brazilian PIX?

Every ton that China pulls from the ground in Hunan or off the Shandong coast is a ton that China’s gold reserves absorb domestically — no sanctions risk, no Western pricing dependency. With BRICS gold accumulation still building month after month, and central bank gold buying across the bloc showing no signs of slowing, this de-dollarization gold shift looks less like a trend and more like a structural reset of how the world holds value.